A UAE Trade License marks the beginning—not the end—of your business journey. Explore the essential operational, financial, and compliance steps every business should take after incorporation to build a compliant, growth-ready, and sustainable organization.

Introduction

Obtaining a UAE Trade License is an exciting milestone for every entrepreneur. It officially marks the beginning of your business journey and gives your company the legal authority to operate within one of the world's most dynamic business environments.

However, from a strategic business perspective, company formation is only the first step.

Once the trade license is issued, businesses enter a new phase that requires careful financial planning, regulatory compliance, operational readiness, and long-term decision-making. While obtaining the license is often the primary focus during company formation, the actions taken immediately afterward play an equally important role in determining how efficiently a business operates and grows.

Understanding these post-incorporation responsibilities can help businesses avoid unnecessary delays, strengthen compliance, improve operational efficiency, and establish a solid foundation for sustainable growth.

Why a Trade License Is Only the Beginning

A trade license legally authorizes a business to operate within the UAE, but it does not automatically prepare the business for day-to-day operations.

Running a successful company requires a combination of financial discipline, regulatory compliance, operational planning, and continuous business management.

Businesses that establish these systems from the beginning are generally better positioned to respond to market opportunities, meet regulatory obligations, and achieve long-term growth.

Simply put, obtaining a trade license starts the business—but structured planning helps sustain it.

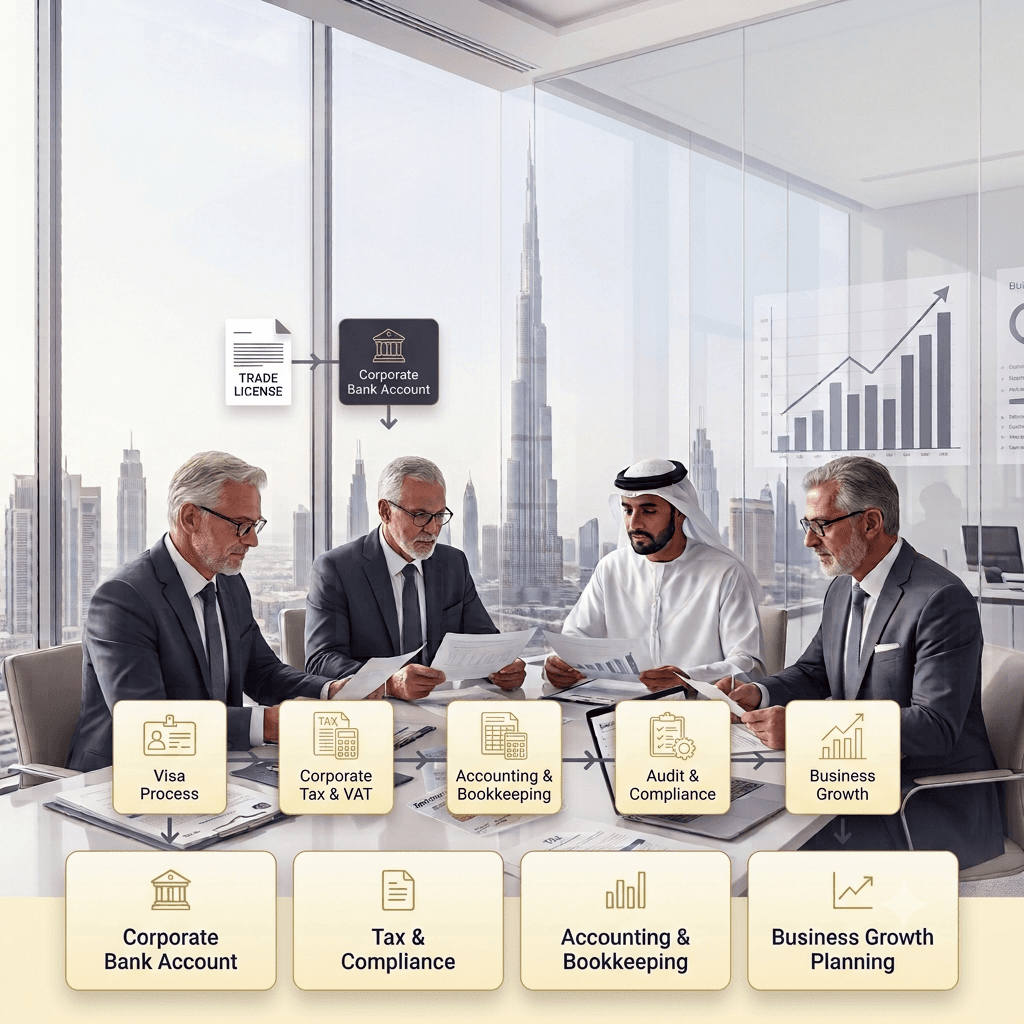

1. Complete Your Visa and Immigration Process

For businesses that have visa eligibility, the next stage involves completing the UAE immigration process.

Depending on the selected package and applicant status, this may include:

Entry Permit (where applicable)

Status Adjustment

Medical Fitness Examination

Emirates ID Registration

Residence Visa Issuance

Completing these formalities enables shareholders and employees to legally reside and work in the UAE.

Planning the immigration process early also minimizes unnecessary administrative delays and allows business owners to begin operations without interruption.

2. Open Your Corporate Bank Account

Many entrepreneurs assume that once the trade license is issued, opening a business bank account is a straightforward process.

In reality, every bank follows its own compliance procedures and risk assessment policies before approving a corporate account.

Financial institutions may request:

Trade License

Memorandum of Association (MOA)

Shareholder documents

Business plan or business model explanation

Source of funds

Expected transaction profile

Information about business activities

Preparing these documents in advance significantly improves the onboarding process.

Choosing the right banking partner is equally important. Businesses should evaluate banking facilities, international transaction capabilities, online banking services, and future financing options before making a decision.

A well-prepared banking application not only saves time but also supports smoother business operations from the beginning.

3. Understand Your Tax and Regulatory Obligations

The UAE's regulatory environment has evolved significantly in recent years.

Today, businesses are expected to understand and comply with various financial and regulatory requirements depending on their activities and applicable thresholds.

These may include:

Corporate Tax Registration

VAT Registration (where applicable)

Ultimate Beneficial Owner (UBO) declarations

Economic Substance Regulations (where applicable)

Anti-Money Laundering (AML) obligations for regulated sectors

Rather than viewing compliance as an administrative burden, successful businesses integrate compliance into their overall business strategy.

Early planning reduces regulatory risks, improves operational confidence, and supports stronger corporate governance.

4. Establish Strong Accounting and Bookkeeping Practices

One of the most common mistakes made by new businesses is delaying accounting until the end of the financial year.

This often results in incomplete records, reconciliation challenges, and unnecessary pressure during tax filing or audit preparation.

Maintaining accurate accounting records from the beginning enables businesses to:

Monitor cash flow effectively

Evaluate profitability

Prepare financial statements

Support Corporate Tax and VAT compliance

Improve budgeting and forecasting

Make informed business decisions

Reliable financial information also strengthens credibility with banks, investors, suppliers, and other stakeholders.

Good bookkeeping is not simply about meeting compliance requirements—it is a valuable management tool that supports sustainable business growth.

5. Build an Audit-Ready Business

Many businesses only think about audits when they receive an audit request.

In reality, audit readiness should be an ongoing business practice rather than a last-minute exercise.

Organizations that maintain structured documentation, reliable accounting records, and effective internal controls throughout the year are significantly better prepared for financial reporting and regulatory reviews.

An audit-ready business typically demonstrates:

Accurate financial records

Proper document management

Consistent accounting practices

Effective internal controls

Strong governance standards

Developing these systems early reduces operational risks and enhances overall business transparency.

6. Maintain Ongoing Compliance

Business compliance is not a one-time requirement.

It is an ongoing responsibility throughout the lifecycle of the company.

Businesses should continuously monitor important obligations such as:

Trade License renewals

Visa renewals

Corporate Tax filings

VAT submissions

Accounting records

Regulatory reporting requirements

Missing important deadlines may result in financial penalties, operational disruptions, or unnecessary administrative complications.

Maintaining a structured compliance calendar allows businesses to stay organized while focusing on growth.

7. Plan for Future Business Growth

Successful businesses rarely remain unchanged after incorporation.

As operations expand, entrepreneurs may require:

Additional residence visas

New business activities

Office upgrades

Branch registrations

Shareholder amendments

Business restructuring

Planning for future expansion from the early stages often reduces costs, minimizes administrative delays, and provides greater operational flexibility.

Growth is rarely accidental—it is usually the result of structured planning and informed decision-making.

8. Develop a Business Continuity and Growth Plan

Receiving a trade license is only the first milestone in your entrepreneurial journey.

As business operations begin, it becomes equally important to establish a roadmap for future development.

Business owners should regularly evaluate:

Operational performance

Financial health

Market opportunities

Customer requirements

Expansion plans

Risk management strategies

Whether the objective is hiring additional employees, expanding into new Emirates, entering international markets, or introducing new business activities, having a structured growth strategy allows businesses to adapt more effectively to changing market conditions.

Organizations that continuously review their objectives and align them with business performance are generally better positioned to achieve sustainable long-term success.

Common Mistakes After Receiving a Trade License

While the responsibilities discussed above may appear straightforward, many businesses encounter avoidable challenges simply because post-incorporation planning is overlooked.

Some of the most common mistakes include:

Delaying the corporate bank account application

Ignoring accounting and bookkeeping until year-end

Missing Corporate Tax or VAT registration requirements

Overlooking license renewal deadlines

Operating without a structured compliance plan

Making business decisions without considering future expansion

Avoiding these challenges can save businesses significant time, cost, and administrative effort.

Why It Matters

A UAE Trade License establishes your business legally.

The systems, governance, and decisions you build afterwards determine how successfully your business operates.

Long-term success is not determined by how quickly a company is incorporated, but by how effectively it is managed after incorporation.

Organizations that invest in compliance, financial management, operational planning, and strategic decision-making are generally better positioned to build resilient businesses capable of long-term growth.

Business success is not simply about starting a company—it is about building one that can adapt, grow, and remain sustainable in an evolving business environment.

How We Can Help

Starting a business is only the beginning of your entrepreneurial journey.

Managing it successfully requires continuous planning, compliance, financial discipline, and informed decision-making.

At Bridgewater Management Consultancies (BWMC), we support businesses beyond company formation by providing practical guidance throughout every stage of their business lifecycle.

Our services include:

Business Setup & Company Formation

UAE Residence Visa Assistance

Corporate Bank Account Assistance

Corporate Tax Registration & Advisory

VAT Registration & Compliance

Accounting & Bookkeeping

Audit & Assurance Services

Business Advisory & Compliance Support

Whether you are establishing your first company in the UAE or expanding an existing business, our team is committed to helping you build a compliant, financially structured, and growth-oriented business.

Contact Us

📧 Sales & General Enquiries: sales@bwmc.ae

📧 Business Consultant: barkha@bwmc.ae

👤 Contact Person: Barkha Singh

📱 Mobile / WhatsApp: +971 543097848

🌐Website:www.bwmc.ae